The Role of Cyber Insurance in Crypto Recovery

Cyber insurance is defined as a financial protection product that covers the costs of responding to a digital breach, including forensic investigations, legal defense, and breach notification. The role of cyber insurance in crypto recovery is specific and often misunderstood: standard policies cover the professional fees required to investigate and respond to theft, not the market value of the stolen cryptocurrency itself. Forensic investigations alone can range from tens of thousands to several hundred thousand dollars depending on breach complexity. That cost exposure is real and significant, even before any legal recovery process begins. Specialized digital-asset policies have emerged to fill the gap, and understanding both product types is the first step toward building a defensible financial protection strategy.

What does cyber insurance cover in a crypto theft?

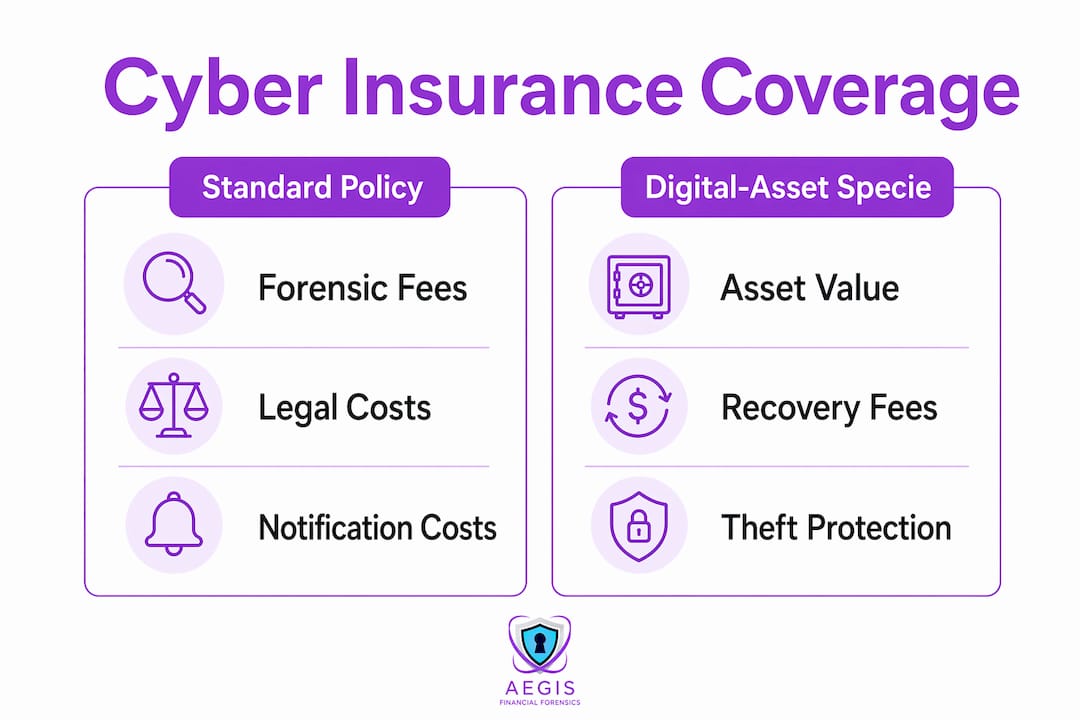

Standard cyber policies exclude the market value of stolen cryptocurrency. They cover breach response costs: forensic investigation, legal defense, regulatory notification, and crisis management. This distinction matters because most policyholders assume their insurer will reimburse the full value of stolen coins. That assumption is incorrect under virtually every standard cyber policy currently available.

The exclusion exists for a specific reason. Insurers classify cryptocurrency as neither traditional money nor recoverable data, which places it outside the scope of standard cyber coverage. Insuring the digital asset itself requires a “specie” or digital-asset comprehensive crime policy, a separate product category with its own underwriting requirements. Without that layer, a business that loses $500,000 in Bitcoin to a phishing attack may receive coverage only for the $80,000 forensic investigation that follows.

| Coverage Item | Standard Cyber Policy | Digital-Asset Specie Policy |

|---|---|---|

| Forensic investigation fees | Covered | Covered |

| Legal defense and recovery costs | Covered | Covered |

| Breach notification expenses | Covered | Covered |

| Market value of stolen crypto | Excluded | Covered (subject to terms) |

| Internal fraud and key theft | Excluded | Often covered |

The table above shows why policy type selection is not a minor administrative decision. It determines whether a theft event results in partial cost recovery or full asset indemnification.

Key exclusions to verify in any standard cyber policy include:

- Value-of-digital-asset exclusions that remove coin market value from coverage

- Custodied client crypto exclusions in commercial crime policies

- Unilateral transfer exclusions that deny coverage for authorized but fraudulent transactions

- Voluntary parting exclusions triggered when a user approves a transaction under social engineering

Are there specialized insurance products for crypto recovery costs?

Specialized digital-asset insurance products now cover the professional fees associated with recovering stolen cryptocurrency, even when they stop short of covering the asset’s market value. Willis Towers Watson’s acquisition of Redefind represents the clearest market signal that institutional demand for this coverage tier is growing. The product category targets the gap between standard cyber policies and full specie coverage.

Focusing coverage on recoverable professional costs rather than volatile asset values produces more stable premiums, which makes these products accessible to smaller investors and mid-market businesses. A policy covering blockchain forensics and legal recovery fees carries a predictable cost basis. A policy covering the market value of Bitcoin does not, because the underlying asset can move 30% in a week.

These specialized products typically cover:

- Blockchain forensic investigation and attribution analysis

- Legal fees for asset freeze applications and court orders

- Coordination costs with regulated exchanges for asset holds

- Regulatory compliance costs triggered by the theft event

- Professional fees for expert witness testimony in recovery proceedings

Legal and forensic recovery proceedings following crypto theft can take between 3 and 18 months and generate substantial professional fees throughout that period. A specialized policy that covers those fees provides meaningful financial protection even without covering the stolen asset’s value.

Pro Tip: Request a specimen policy wording from any insurer offering digital-asset coverage. Compare the definition of “digital asset” and the scope of “professional fees” line by line before binding coverage. Vague definitions create claim disputes.

What are the main challenges in recovering stolen crypto?

Blockchain transaction irreversibility is the primary barrier to crypto recovery. Once a transaction is confirmed on-chain, no central authority can reverse it. Recovery depends entirely on legal intervention at regulated exchange points where stolen assets can be frozen before conversion or withdrawal.

Rapid detection and coordinated legal action are critical to maximizing asset recovery chances after a theft event. The clock starts immediately. Stolen cryptocurrency moves through mixers, bridging services, and layered wallet structures within hours of the initial theft. Recovery success rates drop sharply after the first 72 hours.

The practical recovery process involves several sequential steps:

- Initiate blockchain forensic tracing within 24 hours to map the transaction path and identify destination wallets

- Engage legal counsel to prepare asset freeze applications for relevant jurisdictions

- Submit formal requests to regulated exchanges holding destination wallets, supported by forensic evidence

- File police reports and regulatory complaints to establish an official record for insurance and legal proceedings

- Coordinate with law enforcement agencies that have jurisdiction over identified exchange operators

- Maintain chain-of-custody documentation for all forensic evidence to support court proceedings

Cyber insurance covers steps 1, 2, and 3 in terms of professional fees. That coverage is material. A blockchain forensic investigation conducted by qualified analysts, combined with legal representation across multiple jurisdictions, routinely generates six-figure professional fee exposure.

Pro Tip: Document every security control in place at the time of theft, including wallet type, access logs, and authentication records. Insurers require this documentation to validate coverage, and courts require it to support asset freeze applications.

How do you select the right cyber insurance for crypto assets?

Crypto-related case law remains minimal, which means policy language carries more weight than judicial precedent in determining claim outcomes. Policyholders cannot rely on established court interpretations to fill gaps in ambiguous policy wording. Every coverage question will be resolved by the policy text itself.

Security protocols directly influence underwriting decisions for crypto-related coverage. Underwriters assess cold versus hot wallet storage ratios, multi-factor authentication implementation, key management procedures, and access control frameworks. Businesses that store the majority of assets in cold wallets with documented key management protocols receive materially better terms than those operating primarily through hot wallets.

Valuation disputes without predefined mechanisms cause claim delays or denials. A policy that does not specify how stolen cryptocurrency is valued at the time of loss creates an immediate conflict when a claim is filed. Including a specific valuation method, such as the weighted average exchange price across major platforms at the time of confirmed theft, eliminates that conflict before it arises.

Key considerations when reviewing any crypto-related insurance policy:

- Confirm the policy contains no blanket value-of-digital-asset exclusion, or that a specie endorsement removes it

- Verify the definition of “professional fees” explicitly includes blockchain forensic services and legal recovery costs

- Confirm the valuation methodology is defined and agreed upon before binding

- Check whether the policy covers theft by internal actors, not only external attackers

- Review sublimits that may cap forensic or legal fee coverage below actual exposure

Working with a broker who has placed crypto-specific coverage is not optional for complex cases. Generic commercial insurance brokers lack the underwriting relationships and product knowledge required to negotiate meaningful terms in this specialty market. The legal cooperation process in crypto recovery is complex enough that policy gaps discovered after a loss event are effectively unrecoverable.

Key Takeaways

Cyber insurance covers the costs of investigating and responding to crypto theft, but recovering the stolen asset’s market value requires a separate specialized policy.

| Point | Details |

|---|---|

| Standard policies exclude asset value | Cyber insurance covers forensic and legal fees, not the market value of stolen cryptocurrency. |

| Specie policies fill the gap | Digital-asset comprehensive crime policies cover theft of the asset itself, including internal fraud. |

| Recovery window is narrow | Forensic tracing and legal freeze requests must begin within 24–72 hours to maximize recovery chances. |

| Valuation language is critical | Policies without predefined valuation methods create claim disputes that delay or deny payment. |

| Security controls affect coverage | Cold wallet storage, multi-factor authentication, and documented key management improve underwriting terms. |

The coverage gap most policyholders discover too late

The most consistent pattern I have observed in crypto theft cases is that policyholders learn about the value-of-digital-asset exclusion at the worst possible moment: when they file a claim. They purchased cyber insurance in good faith, assumed it covered their digital assets, and discovered the exclusion only after the loss occurred. That sequence is not a failure of the insurance market. It is a failure of pre-purchase due diligence.

The emerging specialized policy tier is a genuine development. Products that cover blockchain forensic fees and legal recovery costs without attempting to price volatile asset values represent a structurally sound approach to this risk category. Premiums are more predictable, underwriting is more consistent, and the coverage aligns with the actual cost exposure that most theft victims face.

The practical implication is straightforward. Any individual or business holding material cryptocurrency positions should conduct an annual policy review that specifically addresses crypto-related exclusions. That review should involve a broker with documented experience in digital-asset placements, not a generalist. The steps to tracing stolen crypto assets are well-established. The insurance infrastructure to fund those steps is still maturing, and policyholders who engage with it proactively will be in a substantially better position than those who do not.

— Escareno

How Aegisfinancialforensics supports crypto recovery and insurance claims

When a crypto theft occurs, the quality of the forensic investigation determines both the recovery outcome and the insurance claim outcome. Weak forensic documentation produces failed asset freeze applications and disputed insurance claims. Thorough, court-ready forensic analysis produces the opposite.

Aegisfinancialforensics has assisted with over $34 billion in illicit funds seized or recovered, working with more than 1,500 clients including major regulators and institutions. The firm’s AI-driven blockchain forensic process traces stolen digital assets across networks, produces evidentiary-grade documentation, and supports the legal recovery proceedings that insurance policies are designed to fund. For individuals and businesses navigating a theft event, the crypto fund recovery investigation service provides the forensic foundation that both courts and insurers require. Consulting with qualified forensic specialists at the earliest stage of a theft event is the single most effective way to preserve recovery options.

FAQ

Does cyber insurance cover stolen cryptocurrency?

Standard cyber insurance does not cover the market value of stolen cryptocurrency. It covers breach response costs including forensic investigations and legal fees, which can range from tens of thousands to several hundred thousand dollars.

What type of insurance covers the actual value of stolen crypto?

A “specie” or digital-asset comprehensive crime policy covers the theft of digital assets themselves. These specialized products are separate from standard cyber policies and require distinct underwriting.

How long does crypto recovery take after a theft?

Legal and forensic recovery proceedings typically take between 3 and 18 months. Recovery success depends heavily on initiating blockchain forensic tracing and legal freeze requests within the first 24–72 hours after theft.

What security controls improve cyber insurance terms for crypto?

Cold wallet storage, multi-factor authentication, and documented key management procedures all improve underwriting terms. Insurers treat these controls as indicators of reduced risk exposure.

Why do crypto insurance claims get denied or delayed?

Claims are most commonly delayed or denied due to ambiguous valuation language in the policy. Policies that do not define how stolen cryptocurrency is valued at the time of loss create disputes that underwriters resolve in their own favor.